Just yesterday Dave Kimbell, the CEO of Ulta [full disclosure: one of Rare Beauty Brands’ largest customers] made comments that precipitated a roughly 15% decline in the company’s stock price, the largest single-day decline in several years. Shares in several other prominent beauty companies saw similar declines in the wake of his remarks.

Specifically, Mr. Kimbell said “What we’re seeing right now, as we’re two months into our fiscal year, we have seen a slowdown in the total category.” He added that this slowdown had occurred “a bit earlier” and been “a bit bigger than we thought,” and that the growth rate had come down “probably faster than we anticipated.” As for the causes of the spending slowdown, he cited, “a soup of activity” that includes inflation on core goods and services, higher levels of credit card debt, the return of student loan payments, the U.S. presidential election this year, and international conflicts.

Personally, I’ve talked to executives in other B2C businesses ranging from beauty to pet to wine & spirits to automotive and the consensus is that after an enormous Q4 in which consumers gorged on a wide variety of products, Q1 has been much slower than almost everyone anticipated. So the good new and bad news, I guess, is that the slowdown does not appear to be limited to a specific product category, retailer or brand – we’re all in this together.

But the obvious question is, “How long will ‘this’ last?” Do we expect that this is the beginning of the much-forecasted-but-not-yet-realized recession that was supposed to hit in 2021 2022 2023? Or do we think that this is a temporary pause before we’re back to the good times again? Obviously the answer to these questions will have direct implications for how we run our businesses.

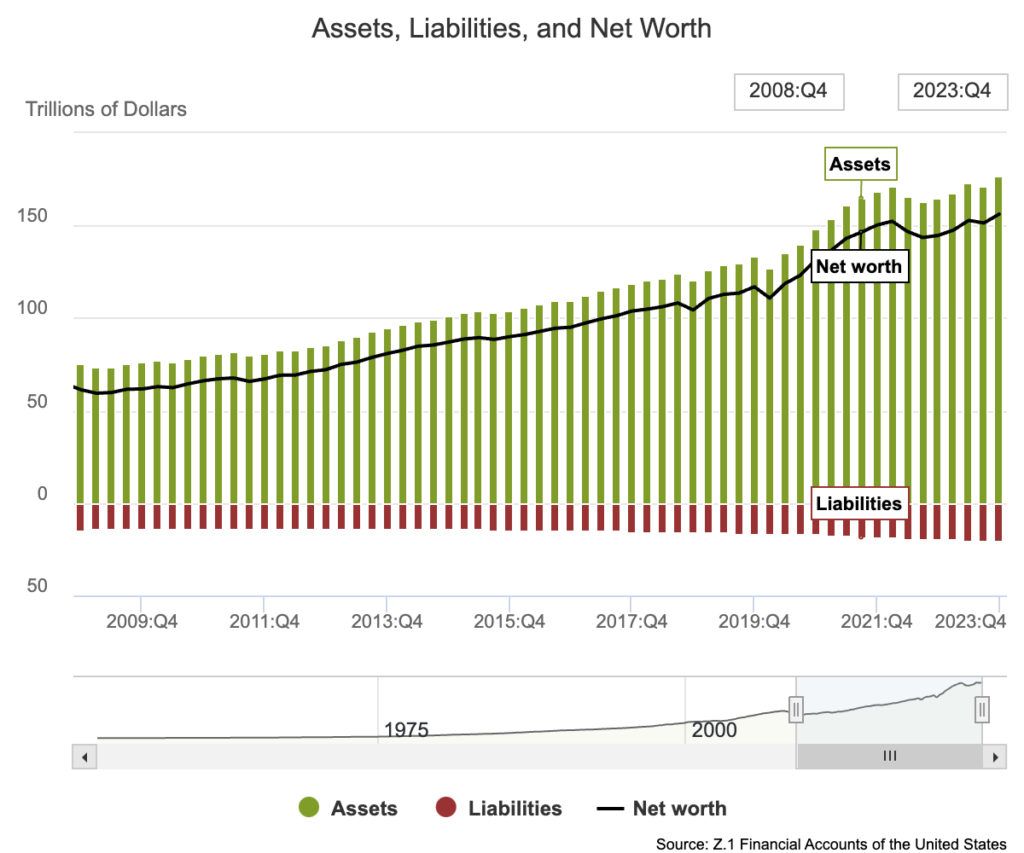

If you just look at the published economic data, you might conclude that the slowdown is just a temporary blip. Inflation has largely abated, though not quite to the 2% Fed target. The unemployment rate is low and real wages are strong – people are working and making money. And consumer balance sheets are strong, with assets far outweighing liabilities (credit: Federal Reserve):

But as Mark Twain famously quipped, “there are three kinds of lies: lies, damned lies, and statistics.” And clearly there’s more to the story if the headline data are strong but individual consumers are pulling back on spending in a wide variety of areas.

I think what’s going on is people are just generally pessimistic right now. They’re frustrated with high prices. They’re tired of our politics, on both sides. They’re scared and disappointed by foreign wars, real and potential. They’re done with (anti)social media. They’re tired of the cold weather. And while their personal situation may be quite comfortable thank you very much, many people believe our society in general is in a funk. She’s no Mark Twain, but as my mother taught me, money can’t buy happiness.

My guess is that consumer spending will rebound from Q1 and remain respectable through 2024 — there IS money out there after all. And I think the upside scenario is that once we get through the election, interest rates start to come down, and we (hopefully) achieve greater stability at home and abroad (2025?), the pessimism will fade and it will once again be ‘game on.’